Bond market Commentary

Declining Credit Creating Opportunities

The U.S. investment-grade (IG) corporate bond market benefits from a sound U.S. Banking sector, good liquidity among highly-rated Industrials, accommodative monetary policy and improved valuations. Key risks include weakening corporate profits, elevated mergers and acquisitions (M&A), debt-funded share buybacks, economic slowdowns in large non-U.S. economies and less constructive market technicals. U.S. economic data also remain mixed with consumer-related segments showing decent growth but manufacturing activities and inflation disappointing. As the Fed gets closer to an albeit delayed liftoff and the credit cycle matures, we expect for the remainder of 2015 a continuation of the volatility experienced in the corporate market year to date. IG corporate spreads have widened 40 basis points (bps) over the last nine months and that has created opportunities to buy bonds from high-quality issuers at more attractive valuations.

Excess Returns Negative in the Third Quarter

Per Barclays, the total return for the intermediate IG corporate bond market was 0.71 percent in the third quarter. Following on a weak second-quarter performance, the intermediate corporate market generated -75 bps of excess return in the third quarter compared to duration-matched treasuries. The intermediate market’s excess return was materially better than the long corporate market, which produced -311 bps. From a quality perspective, AA-rated intermediate corporates outperformed the market’s excess return by 54 bps. Lower quality BBB-rated corporates underperformed the corporate market by 65 bps.

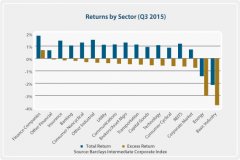

High Variation in Excess Returns by Sector

There was some high sector-level variation in excess returns during the quarter. Financial sectors outperformed based on stable credit fundamentals and low event risk. Consumer noncyclical outperformed on their defensive features and higher credit quality. Energy and basic industry sectors underperformed materially due to weak commodity prices.

There was some high sector-level variation in excess returns during the quarter. Financial sectors outperformed based on stable credit fundamentals and low event risk. Consumer noncyclical outperformed on their defensive features and higher credit quality. Energy and basic industry sectors underperformed materially due to weak commodity prices.

Spreads Wider on Slower Global Growth

In a volatile period, intermediate corporate spreads widened 25 bps ending the third quarter at 144 bps. Slower global growth and weaker commodity prices were the primary drivers of the underperformance. A big new issue calendar and declining credit quality also played a role. Intermediate spreads held up slightly better than long spreads in the quarter. We expect corporate spreads to retrace some of their recent widening as the pace of new IG issuance slows heading into year-end. Spreads are now slightly wide to their long-term median and we think valuations among higher quality corporate bonds are becoming more attractive.

New Issuance and M&A Remain Elevated

New U.S. IG corporate bond issuance of $291 billion in the third quarter was up 25 percent year over year. M&A activity and shareholder enhancements continue to drive the new issue calendar. Several corporate bond mega-deals of $10 billion to $20 billion added to record supply totals. The largest third-quarter deal was Charter Communications Inc.’s .5 billion, M&A-related bond issue. New issue concessions reached levels last seen during the Taper Tantrum of July 2013, as increased volatility and elevated supply caused new issues to price well wide to existing secondary spreads.

A Look at What’s Changed

In our Credit Trends Dashboard, we capture key drivers of IG corporate credit, as well as our view of the incremental shifts in these drivers from quarter to quarter. We made four adjustments to our Dashboard this quarter. Overall, we see IG corporate credit fundamentals as more challenged over the short to medium term.

Key credit drivers that changed during the quarter:

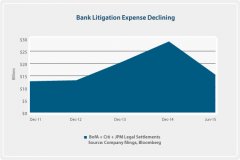

- Litigation Expense: We upgraded our assessment of this driver from modest weakness to neutral. Litigation expenses may have peaked among universal banks. Due to their high frequency, investors also appear to be discounting these large legal settlements.

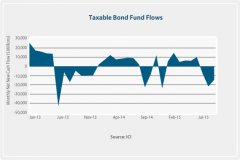

- Fund Flows/Technicals: We downgraded our assessment of this driver from modest strength to modest weakness. Outflows in taxable bond funds picked up in third quarter. Bond liquidity is compromised and the IG supply overhang is high.

- Corporate Profits: We downgraded our assessment of this driver from modest weakness to moderate weakness. S&P 500 second-quarter earnings declined by -0.7 percent per FactSet, and S&P third-quarter earnings are forecast to decline by -4.7 percent.

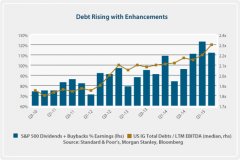

- Operating Trends. We downgraded our assessment of this driver from neutral to modest weakness. Organic revenue and profit growth are weak. Moreover, debt growth is outpacing earnings before interest, taxes, depreciation and amortization (EBITDA) and free cash flow growth.